Jessie Moore has been writing professionally for nearly two decades; for the past seven years, she's focused on writing, ghostwriting, and editing in the finance space. She is a Today Show and Publisher's Weekly-featured author who has written or ghostwritten 10+ books on a wide variety of topics, ranging from day trading to unicorns to plant care.

Managing money is tough and tedious, but technology is here to help.

Sure, you could break out an old-school spreadsheet, but it’ll likely take much longer (and increase your odds of errors) versus a tailor-made personal budget software.

And here’s the best part: Some of the best personal finance software is actually free!

Whether you’re interested in investing, budgeting, or defeating debt, there are plenty of great tools you can download and use today.

What are you waiting for? Let’s review the best personal finance software in 2025.

The best personal finance software in 2025 is…

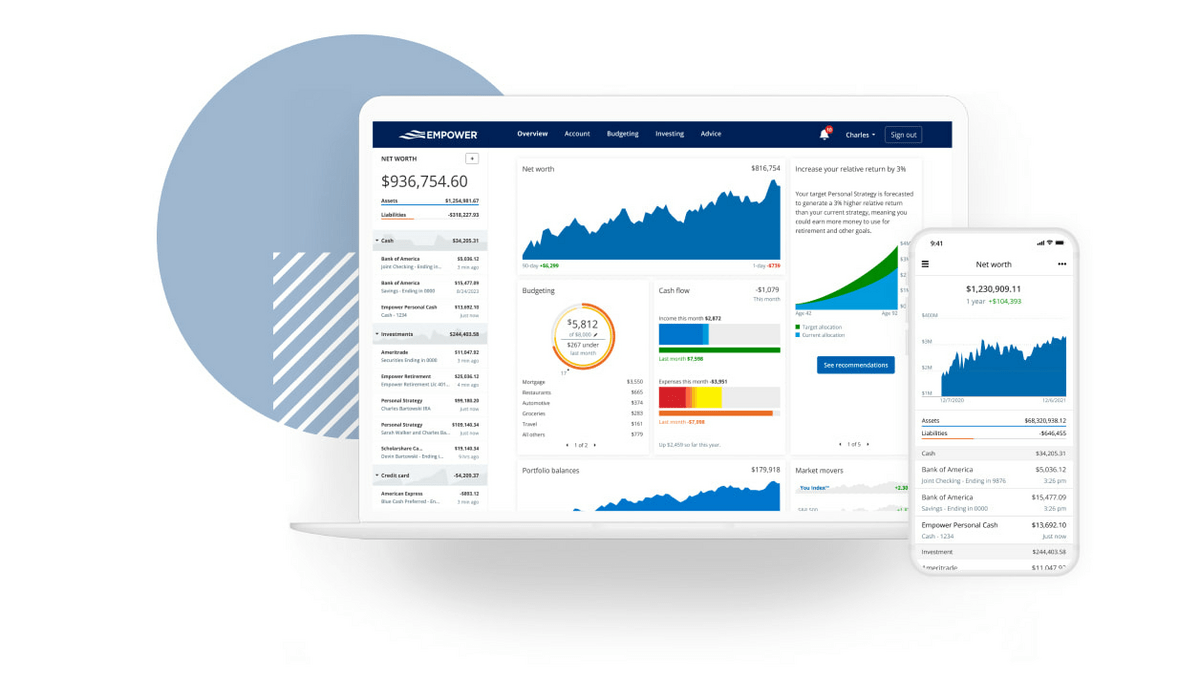

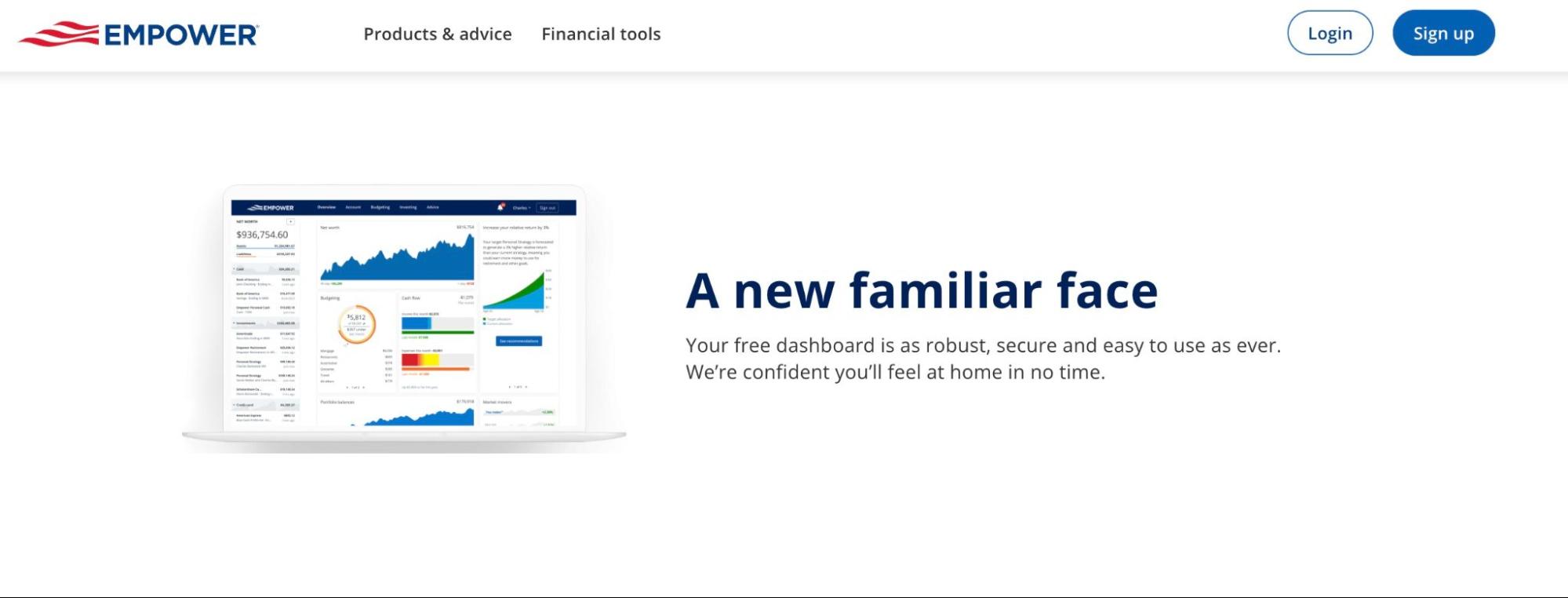

Empower. And it’s free.

Empower’s free dashboard gives you a comprehensive picture of everything from your current budgeting to your total net worth and even forecast your retirement, education, and savings goals.

Empower may not be for individuals who have more advanced accounting needs (for that, we recommend Quicken or Quicken Simplifi), but for the majority of users, it’s the best place to get started.

What to Look for in Personal Finance Software

When looking for the best money management software, first consider your objectives.

While many of the best personal finance software apps offer multiple features, they usually target one area of your financial life.

For instance, some sites offer rockin’ retirement planning dashboards, while others focus on helping you budget better.

Take a moment to list your financial priorities and see which of the best money management software tools offers the solutions you need.

After figuring out your “why,” keep this shortlist in mind when evaluating the best personal finance software:

- Security features: Since you’ll share personal details with these financial tools, please ensure the provider has an A+ reputation for securing user data and meets world-class encryption standards.

- Integrations: Even if one platform is known as the best personal finance software, it won’t help if it doesn’t link to your bank. Check the list of verified partners to make sure your personal finance software can track every account.

- Ease of use: The point of using personal finance software is to make monitoring funds easier, so don’t bother with a tool with a clunky layout.

- Cost: Although some top-notch home budget software solutions are free, their features might not meet your needs. If you’re considering a paid subscription, run a quick cost-to-benefit analysis to see if it’s worth it in the long run.

The Best Personal Finance Software Platforms in 2025

1. Empower (Formerly Personal Capital): Best Overall

- Cost: Free

- Who it’s best for: Anyone looking for a free, comprehensive financial tracking tool

Pros | Cons |

Free to use | Tailored for retirement planning |

Comprehensive suite of tools for budgeting and saving | Might be overwhelming for newcomers |

Automatically syncs with Empower’s other investment services | May receive calls from Empower for accounts over $100,000 |

Integration with advisory services |

Overview:

Empower is best known for its retirement planning services, but in 2023, it instantly became one of the leading apps for comprehensive financial planning. Why?

That’s the year Empower formally re-branded the wealth management suite Personal Capital.

Many of the features formerly on Personal Capital are still here today. They’ve just been given new names or enhanced features thanks to Empower’s superpowers.

On Empower’s extensive dashboard, you can see the full picture of everything from your current budgeting to your total net worth and even forecast your retirement, education, and savings goals.

Besides being a comprehensive tool, Empower is arguably the best personal finance software because it’s free! You’re not obligated to use Empower’s wealth planning services to take advantage of this app.

Key features:

- Budget Planner: Analyze spending and savings trends, set targets, and customize your transactions for more convenient and strategic planning.

- Net Worth: This is the full value of all your assets, including cash, investments, and mortgages.

- Investment Checkup: See how your portfolio stacks up against major indexes like the S&P 500 and monitor the performance and risk of your holdings.

- Retirement Planner: Get a projected portfolio value and see how long it’s likely to take to meet your retirement goals.

- Education Planner: Set a target goal for expected future tuition costs so you stay on course to fund higher education.

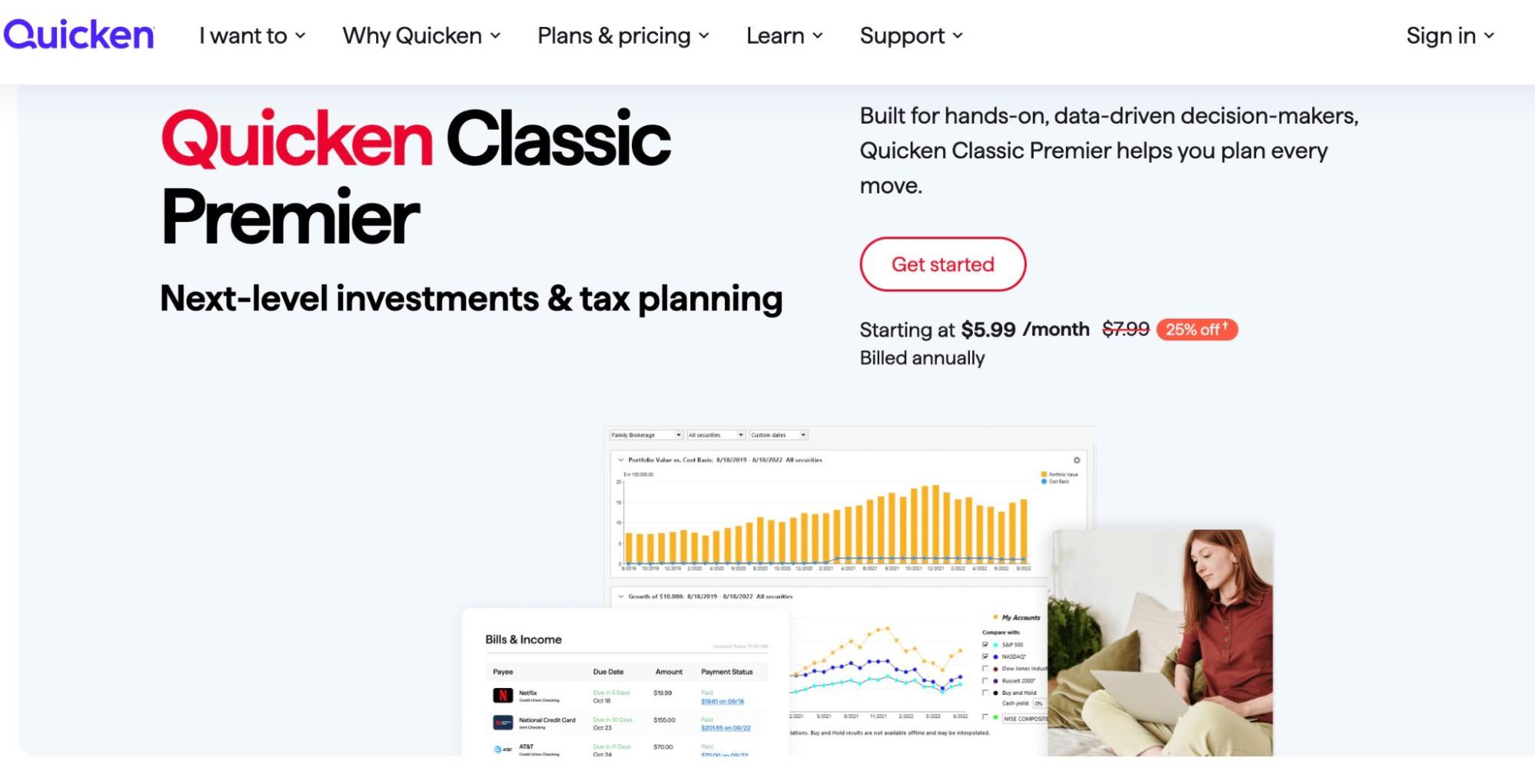

2. Quicken: Best For a Comprehensive Budget, Investment, and Tax Tool

- Cost: Quicken Classic $5.99 per month; Quicken Classic Business & Personal $8.99 per month

- Who it’s best for: People who want a broad financial health overview.

Pros | Cons |

Provides full picture into budget, investing, and savings goals | No free plan available |

Tools to help analyze and manage debt, plus tax tools and integrations | Quicken Classic is desktop-centric |

Long history (dating back to 1984) | Some complaints about UI/UX and errors with categorizing transactions |

30-day money-back guarantee | Requires slightly higher learning curve |

Overview:

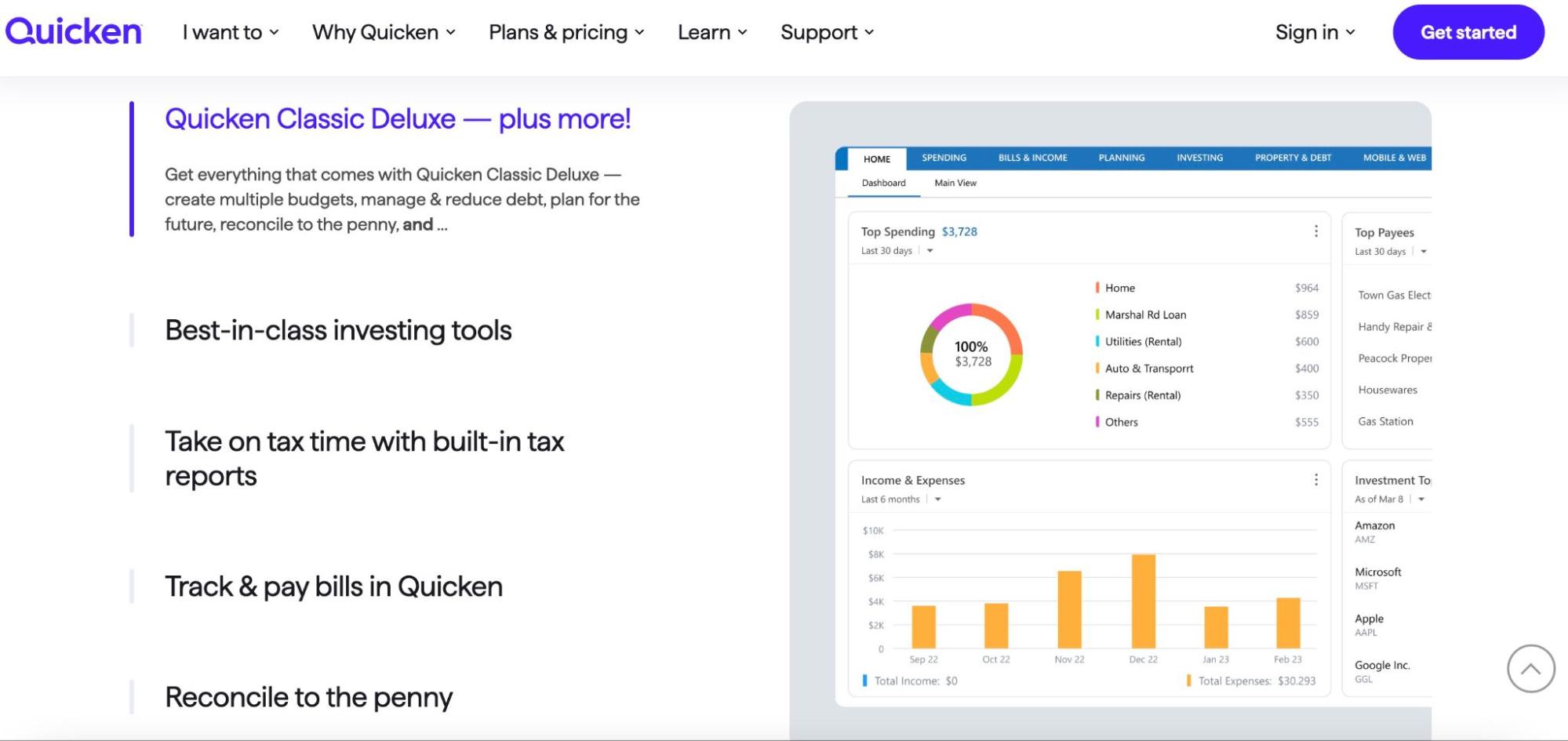

Quicken is largely considered the best personal accounting software out there. With a history going back to the 1980s, Quicken is an OG personal budget software that continues to rank high on lists of the best money management software.

Reviewers and users praise Quicken as the best personal accounting software due to its wide array of integrations and analytics, ranging from retirement planning and investment insights to budgeting tools and debt management.

Although Quicken is comprehensive, it’s not the most user-friendly option and doesn’t offer auto-generated spending plans.

Instead, you’ll have to feel comfortable categorizing your spending and inputting data.

Still, if you want the fullest picture of your finances and don’t mind the extra cost (both in terms of time and money), this is one of the most affordable options for a full-picture personal budget software.

Key features:

- Custom Savings Goals: Design and monitor multiple goals for emergencies, education, vacations, and more.

- Fiscal and Calendar Year Budget: See where your money goes each quarter to handle your expenses better.

- Debt Management: Set goals for paying down debt and review “What-If” suggestions to get closer to financial independence.

- Investment Portfolio Tracker: Follow the real-time value of your investments to ensure they’re hitting your growth expectations.

- Projected Cash Flows: Review a forecast on your income and expenses to see how they impact your goals and balances.

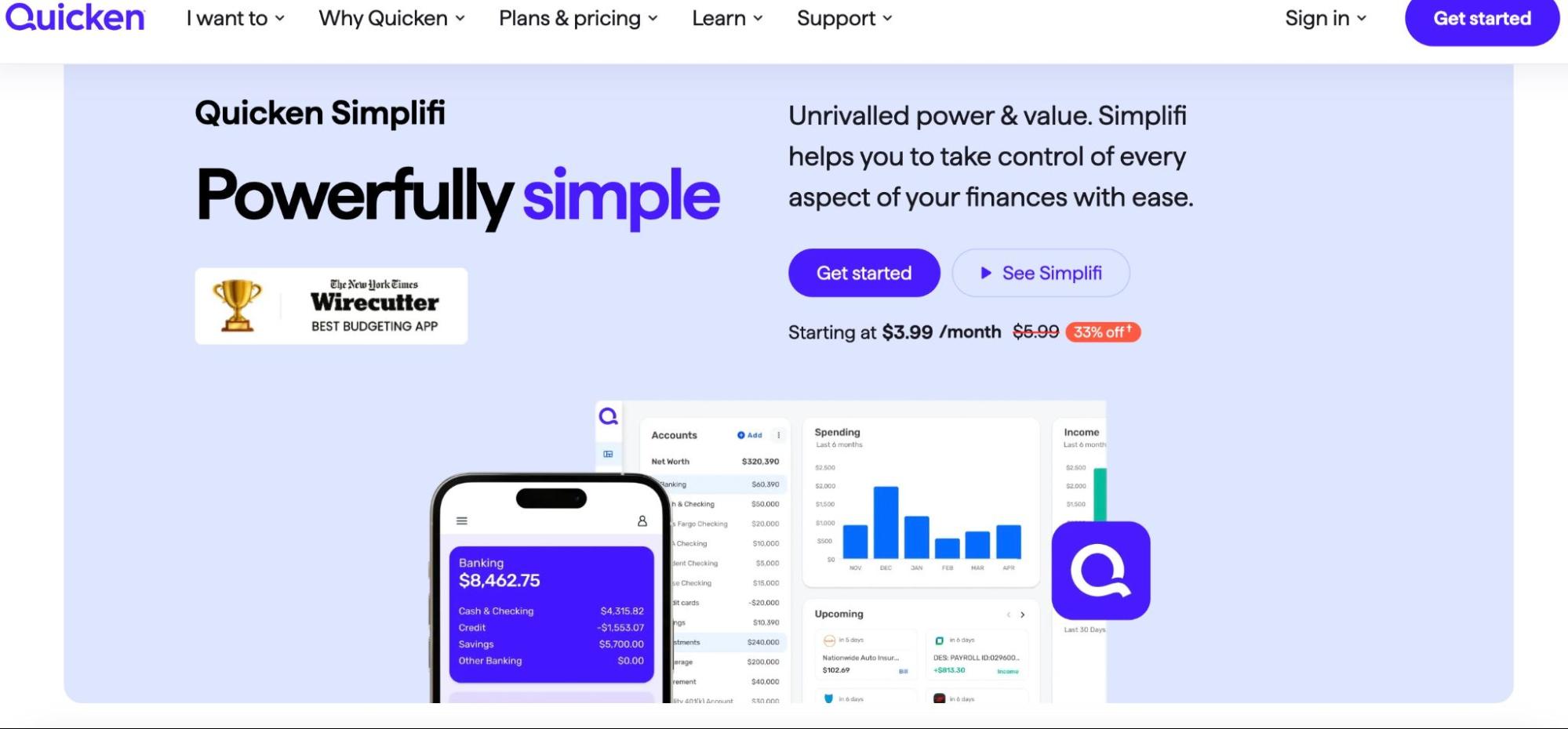

3. Quicken Simplifi: Best for a User-Friendly Overview of Finances

- Cost: $3.99 per month (paid annually)

- Who it’s best for: People looking for an affordable, all-around view into their finances

Pros | Cons |

User-centric platform for desktop and mobile app | No free plan |

Gives complete overview of financial health | Not as many built-in tax integrations versus Quicken |

Built-in cloud storage | Doesn’t include “What-If” tools for debt and investment planning |

Free phone and chat support | Fewer details on investments versus Quicken |

Overview:

That’s right: Quicken is on the list twice. It isn’t content with its status as the classic personal budget software; in 2020, they released the “Simplifi” suite, which they claim is “best for most people.” Let’s talk about why.

For those who find Quicken’s features too overwhelming, the Simplifi app offers a similarly comprehensive experience without needing as much manual input and customization.

You’ll miss out on some of Quicken’s detailed analysis, but Simplifi gives you a good overview of your financial health in convenient mobile and desktop settings.

Plus, auto-generated features like spending plans and bill alerts can help pinpoint budgeting hacks without combing through your expenses.

So, if you’re willing to trade away tax services and customizability for an automated, mobile-friendly experience, Simplifi may “simplify” your life!

Key features:

- Auto-Generated Spending Plan: Review a personalized plan for spending funds using data from your average income and expenses.

- Autodetect Bills and Subscriptions: Check for any expenses you don’t remember or might be paying more than expected.

- Custom Spending Watch Lists: Automatically alerts you if you’re getting close to a pre-programmed spending target.

- Track Upcoming Payments and Impact: Plan ahead for payments and see how your spending patterns affect your overall cash flow.

- Set Goals and Track Debt: Stick to a steady repayment schedule to minimize debt as fast as possible.

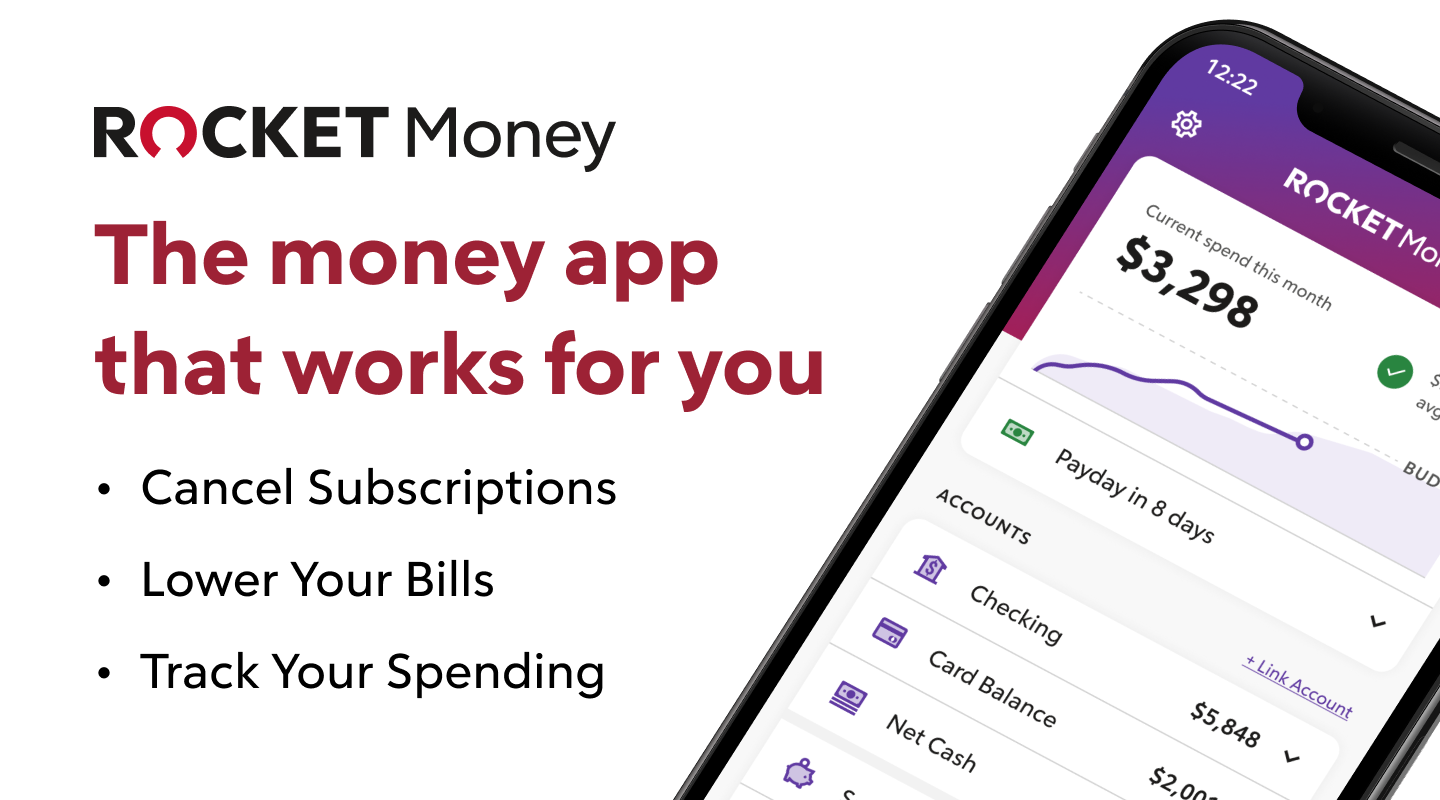

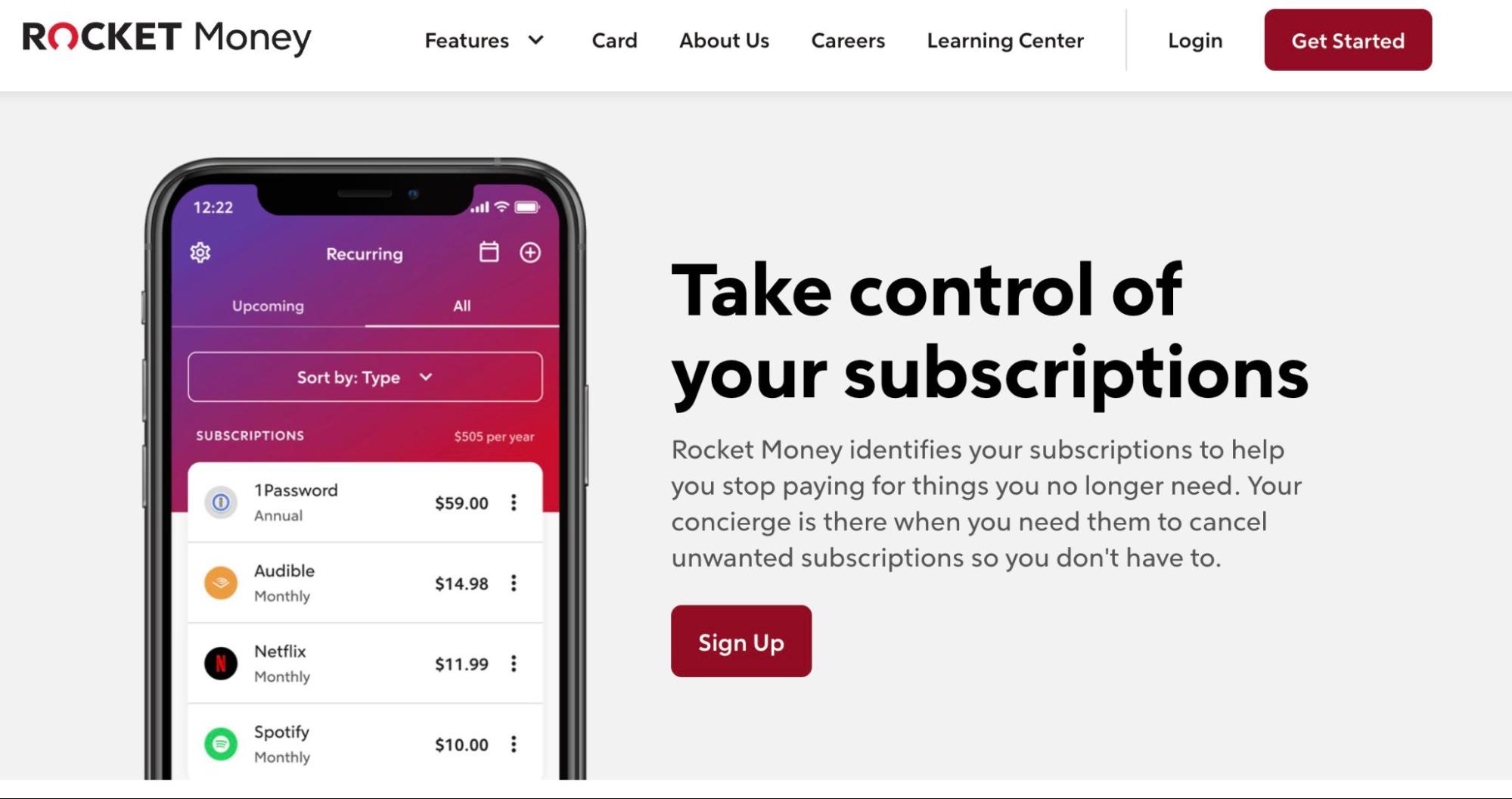

4. Rocket Money: Best For a Hands-Off Approach to Personal Finance

- Cost: Premium costs $6 – $12 per month depending on features you want; Bill negotiation costs 35% – 60% of first year’s savings.

- Who it’s best for: Anyone who wants a more passive approach to monitoring and saving money.

Pros | Cons |

Automatically cancels subscriptions or negotiates bills on your behalf | Steep fee for bill renegotiation |

Offers a broad view into budget and net worth | Lack of transparency on pricing (which triggered a formal CFPB complaint) |

Clean and intuitive interface | Free version is extremely limited |

BBB-accredited with an A+ rating | No phone support |

Overview:

If you aren’t jiving with what Simplifi’s supplying. Rocket Money may be more your style.

Formerly known as Truebill, this personal finance app offers a similarly broad view of your finances with sleek charts and a mobile-friendly UI/UX.

A big feature that sets Rocket Money apart is how it tackles subscriptions and bills.

Instead of merely monitoring these common money drains, you can use your Rocket Money app to delete or renegotiate contracts.

That’s right, Rocket Money’s team will call on your behalf to slim your bills — but you will have to pay a hefty percentage for this service (quoted at 35% – 60%).

Speaking of prices, while Rocket Money offers a free version, you’ll need a paid Premium account to access all of its services.

Although Rocket Money is pricier than Simplifi, the extra cost may be worthwhile if you think the conveniences of subscription cancellation are justified.

Key features:

- Track Subscriptions: Never be in the dark on every monthly subscription that’s taking your money.

- Cancel Unwanted Subscriptions: One of Rocket Money’s key features is that it lets you cancel those naughty subscriptions you forgot about with one click.

- Monitor Credit Score: See which way your credit score is heading and get notified of any significant alerts in your Rocket Money app.

- Bill Negotiation: Don’t like haggling for a lower rate? Rocket Money can negotiate bills for you (provided you don’t mind paying a percent of the projected savings).

- Net Worth Calculator: Rocket Money pulls together all the data on your income, expenses, and debt to provide a clear view of your current net worth.

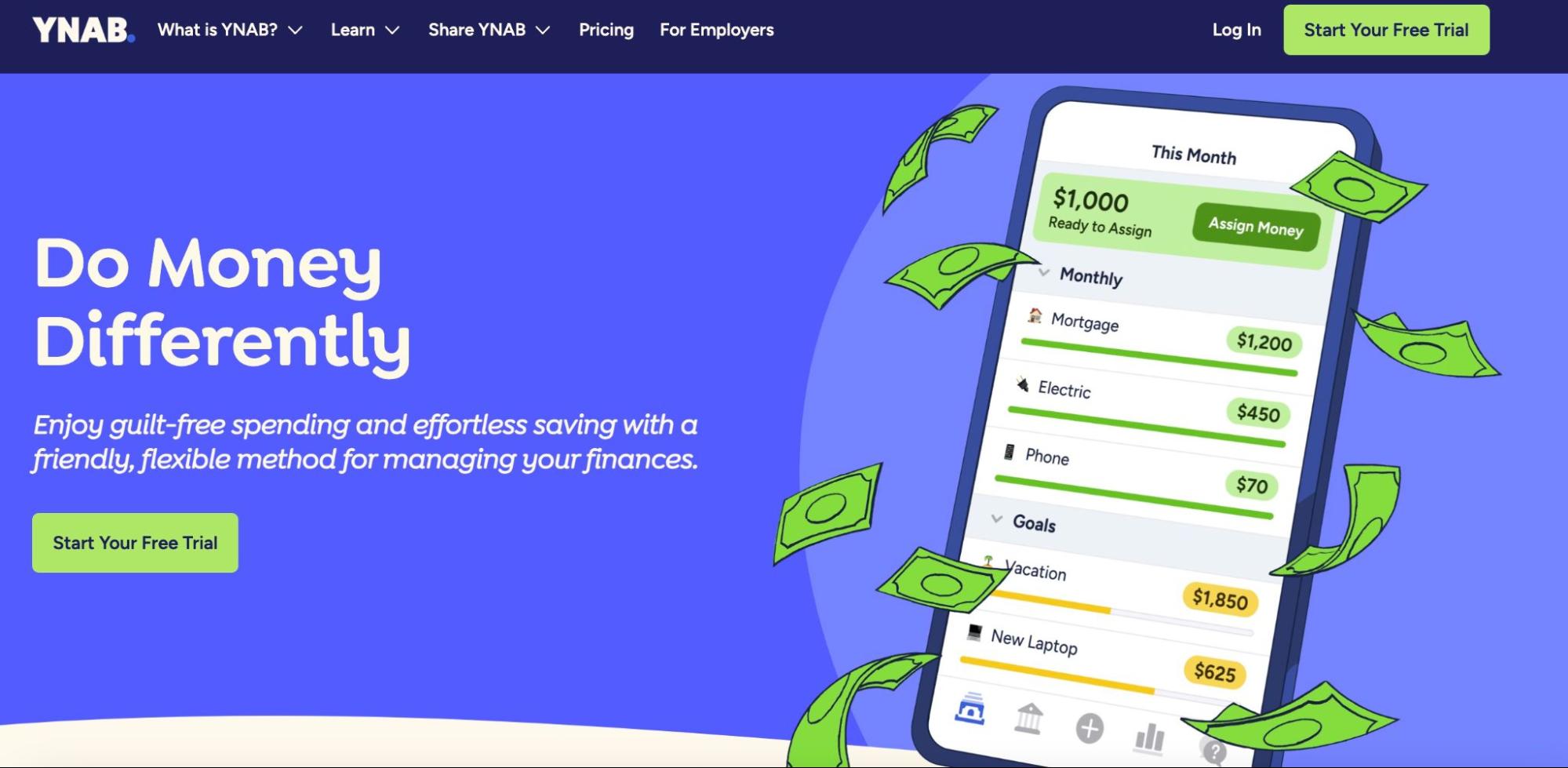

5. YNAB (You Need a Budget): Best For Active Investors

- Cost: $14.99 per month or $109 per year.

- Who it’s best for: People looking to change their relationship with budgeting and are willing to take a more active approach.

Pros | Cons |

Encourages proactive money management | No free plan |

Offers 34-day free trial | Requires active participation and adherence to zero-based budgeting |

Loan calculator and net worth tracker with highly visual graphics | Steeper learning curve |

Extensive educational hub | Doesn’t offer a detailed view into investments, taxes, or retirement planning. |

Overview:

YNAB takes a refreshing, hands-on approach to managing money based on the core philosophy of “zero-based budgeting.”

In summary, this strategy focuses on putting every dollar of income into specific expenses, savings, or debt payments so that nothing is unaccounted for at the end of each budget period.

YNAB puts this theory into practice by setting up a color-coded dashboard with all your savings goals and expenses plus cash as it comes in.

While this strategy demands active involvement, fans of YNAB claim it helps them (literally) view money differently.

Once money arrives in your account, you’ll “assign” it to different tasks—whether short-term or long-term—each month. The point is to ensure every dollar has a clear purpose and that as many of those tasks turn “green.”

Some people find YNAB addicting and fun, but others might find this constant game a time drain.

Also, while YNAB shines as a budgeting tool, it does not provide a long-term view into investments or retirement funding.

However, if you feel you need to drastically change how you manage money, YNAB may be the right virtual “boot camp.”

Key features:

- Monthly Expenses: On YNAB’s dashboard, you’ll assign inflows to different expenses, always ensuring every dollar has a role in your financial life.

- Savings Targets: Seamlessly bring non-monthly expenses and “surprise payments” into your monthly budget by setting longer-term targets.

- Loan Calculator: Explore multiple paydown options with graphs that consider your monthly budget and different debt management scenarios.

- Net Worth Tracking: Download organized graphs and pie charts representing your net worth to get an overview of your progress and areas for improvement.

- Education Hub: Learning about YNAB’s philosophy is essential to getting the most out of this platform, and they provide many resources to help you adapt to this new way of thinking.

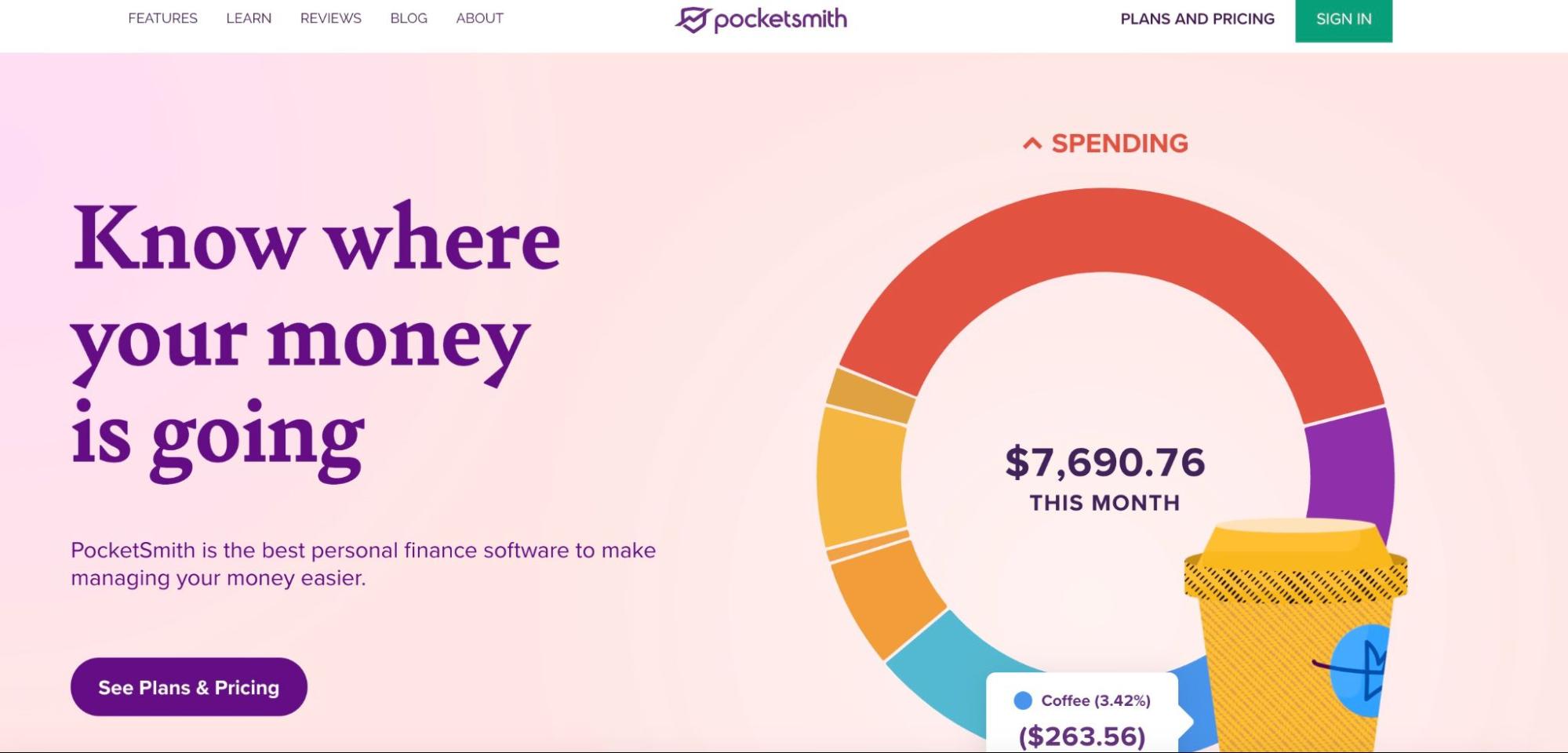

6. PocketSmith: Best For Planning Ahead for Payments

- Cost: Free; $9.99 per month (yearly fee) for Foundation; $16.66 per month (yearly fee) for Flourish; $26.66 per month (yearly fee) for Fortune

- Who it’s best for: People who need extra help planning ahead

Pros | Cons |

Offers a free plan without ads | No automatic feeds for free plan |

Creates organized graphs for easy analysis | Doesn’t track investments |

Calendars to help plan ahead for spending | Paid versions are pricey |

Overview:

PocketSmith may be the best personal finance software if you want to feel prepared for each month’s bills.

Why?

Well, this home budget software took a unique approach by focusing on using a calendar design to organize and visualize your expenses.

While this handy budget calendar is one of PocketSmith’s major perks, it also aggregates all of your banking info to give you a deeper look into your net worth.

PocketSmith’s pretty charts and tables allow you to project future cash flows using current data.

While PocketSmith offers a free version, you’ll have to enter all your banking info manually, and it’s pretty limited in terms of budgets and projection time horizons.

Also, PocketSmith won’t give you a complete picture of your net worth since it doesn’t track investments.

However, if you like PocketSmith’s free version, it might be worth checking out this app’s paid tiers.

Key features:

- Budget Calendar: Pull out this user-friendly, color-coded calendar to keep tabs on your expenses and feel ready for the next bill day.

- Cash Flow Forecasting: Use daily, weekly, and monthly cash flow data to get a sense of your future financial trajectory.

- Net Worth Tracker: See a tally of your assets and liabilities in one convenient screen, including your debts, car, and home.

- Activity Dashboard: Design dashboards for different activities or other people to get a more detailed look into how your money moves.

- Income and Expense Report: Get a closer look into your gains and losses in different categories and export this data to a spreadsheet for further research.

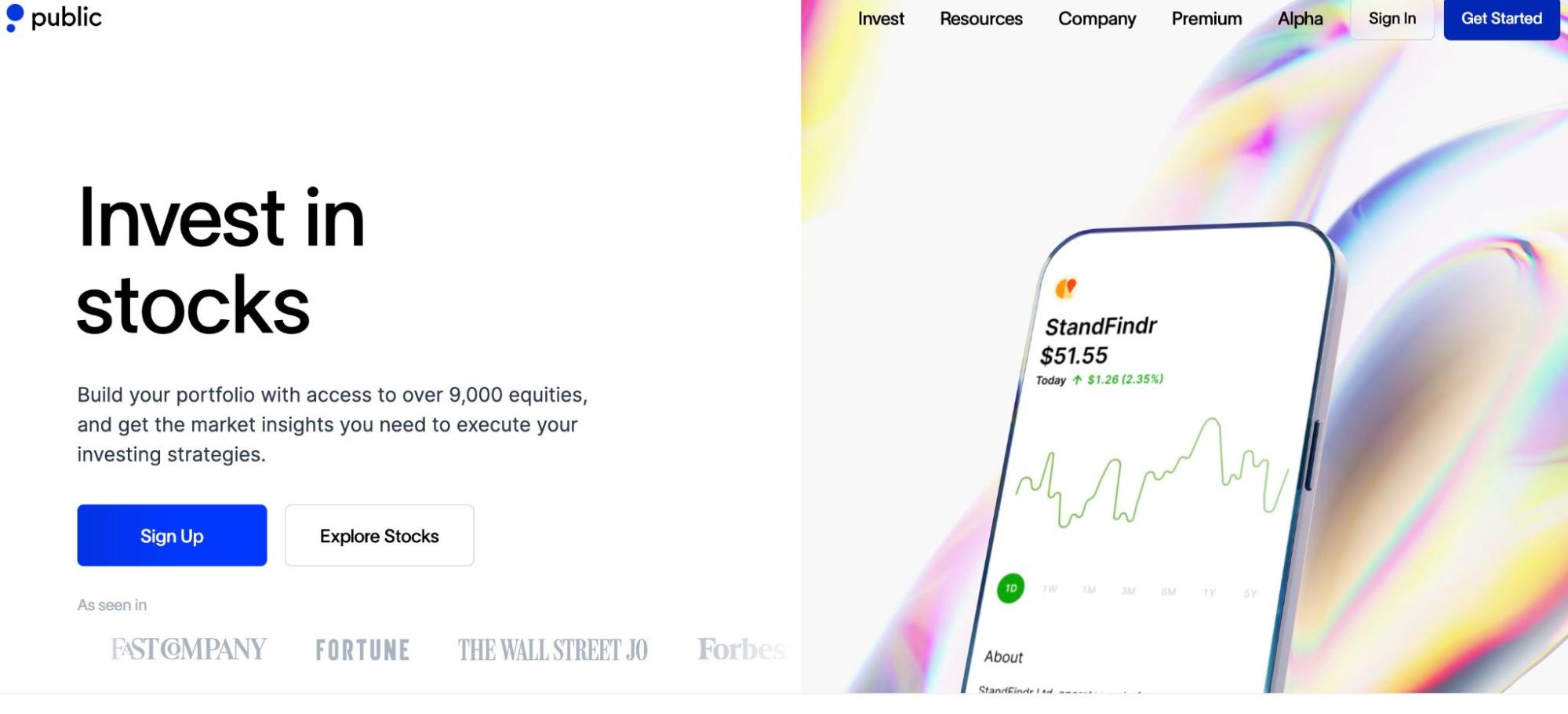

BONUS: When You’re Ready to Invest: Public

- Cost: Free to sign up; Commission-free stock and ETF trading; Trading fees apply for other products like options and crypto.

- Who it’s best for: People who want all their investments in one place

Pros | Cons |

Offers FDIC and SIPC insurance protections | One of the newer fintech platforms (founded 2019) |

Passive income through high-yield savings, treasuries, or bonds | No paper trading for practice |

Commission-free trading for stocks and ETFs | Trading fees for most alternative assets and options |

Innovative options like collectibles, royalties, and crypto | Doesn’t offer mutual funds |

Overview:

If you’re looking for a personal budget software strictly for monitoring your finances, then Public.com probably isn’t the best choice.

Why?

Unlike options like Quicken or Empower, Public is an all-in-one trading and investing app.

On the positive side, this makes Public convenient if you plan to do all your investing in one place.

However, you can’t link other accounts to Public to get an overall picture of your net worth.

Also, Public doesn’t offer budgeting tools and forecasts you’ll find in dedicated personal budget software options.

Still, if you’re looking for a reputable broker that handles pretty much every asset category — including alternatives and income opportunities like high-yield savings — then Public could help you monitor your investments in one dashboard.

Key features:

- Stock and ETF trading: Swap shares of your favorite companies and ETF portfolios without paying commissions.

- High-Yield Cash Account: Earn a higher-than-average interest rate in an FDIC-insured cash account.

- Bond Portfolio: Lock in the latest interest rate for years with Public’s corporate bond portfolio.

- Cryptocurrency Trading: Invest in coins and tokens like Bitcoin and Ethereum through the third-party service Bakkt.

- Options Trading: Speculate on prices or hedge long-term portfolios with put and call options.

- Alternative Assets: Own shares in out-of-the-box asset categories, including collectibles and music royalties.

Final Word:

Whether you download a personal finance software or you’re comfortable cranking out your calculator, you can’t maximize your financial health without knowing your cash flows.

The best personal finance software tools make it easier to take control and save money in the long run.

So, if you don’t notice your finances improving when using one of these apps, chances are you haven’t found the right one.

Take time to test different home budget software apps till you find the one that clicks with your financial journey.

FAQs:

What software to use for personal finance?

While you could use old-school methods like spreadsheets, there are special personal finance software apps like Quicken, Simplifi, and Empower that offer detailed views of your financial life.

What is the most used software in finance?

Due to its longevity, Quicken may be the most respected personal finance software, but other apps like YNAB, Simplifi, and Rocket Money have millions of downloads.

What is the best free accounting software for personal use?

Currently, Empower is the most attractive free personal finance software, thanks to its high reputation and multiple features, including a retirement calculator, budgeting tools, an investment check up tool, and more.

Is there a better program than Quicken?

Quicken has one of the longest reputations as the best personal finance software, but it's not the right fit for every person. Explore more user-friendly options like Empower, Simplifi, or Rocket Money to find what most aligns with your needs.

Where to Invest $1,000 Right Now?

Did you know that stocks rated as "Buy" by the Top Analysts in WallStreetZen's database beat the S&P500 by 98.4% last year?

Our April report reveals the 3 "Strong Buy" stocks that market-beating analysts predict will outperform over the next year.