Jessie Moore has been writing professionally for nearly two decades; for the past seven years, she's focused on writing, ghostwriting, and editing in the finance space. She is a Today Show and Publisher's Weekly-featured author who has written or ghostwritten 10+ books on a wide variety of topics, ranging from day trading to unicorns to plant care.

If you’ve been keeping an eye on ways to supercharge your retirement, you’ve probably come across Self-Directed IRAs (SDIRAs).

They offer all the perks of a conventional IRA … plus the freedom to invest in almost anything under the sun, from real estate to precious metals, private equity, and even cryptocurrency.

One of the most well-known names in the SDIRA space is The Entrust Group.

But is The Entrust Group legit — and is it right for you?

The bottom line? Yes, The Entrust Group is legit. It’s been around for over four decades, boasts billions in assets under administration, and enjoys a solid reputation for helping investors take control of their retirement through self-directed IRAs.

Below, I’ll walk you through everything you need to know: What The Entrust Group offers, how its fees stack up, and how to decide if it’s right for you.

What is The Entrust Group?

The Entrust Group is a financial services company specializing in self-directed retirement accounts. Unlike traditional IRA providers that limit your assets to publicly traded securities, Entrust enables you to invest in just about anything the IRS allows.

Interestingly, The Entrust Group is a bit of a pioneer. Founded in 1981 by Hubert Bromma, Entrust was one of the first custodians to challenge the norm that IRAs must be limited tostocks and bonds.

Bromma believed individual investors should have the freedom to invest in real estate, private equity, and other “alternative” assets — especially if they had specialized knowledge in those areas.

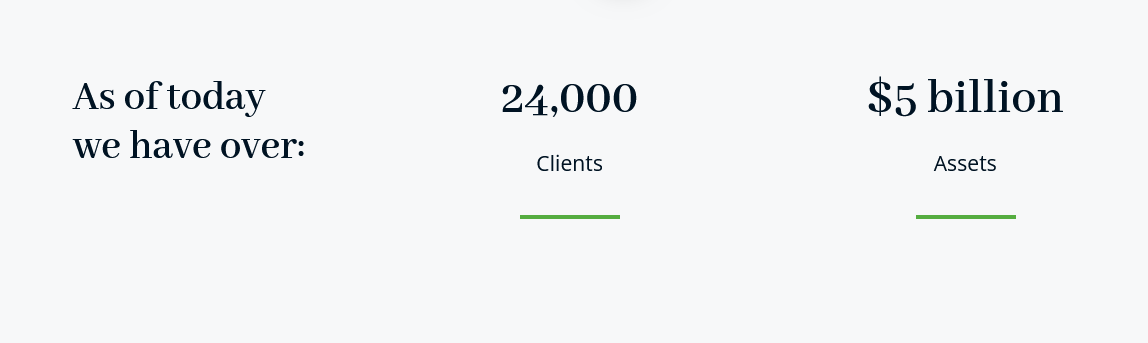

Over the years, The Entrust Group has grown significantly, now serving more than 24,000 clients and holding over $5 billion in assets. They’ve become recognized as a go-to resource for anyone seeking to break free from the limitations of a standard IRA.

Who Does The Entrust Group Serve?

- Real Estate Enthusiasts: If you’ve always dreamt of flipping homes or renting out vacation spots, you can do it inside an IRA (and reap those sweet tax benefits).

- Alternative Asset Fans: From crypto to farmland, many people turn to Entrust because they want alternatives to the public markets.

- Seasoned DIY Investors: If you’re comfortable doing your own due diligence, a self-directed approach can be exhilarating.

Because of the hands-on nature of these investments, most Entrust clients are somewhat experienced.

That said, the company’s educational resources make it accessible for the more adventurous beginners too — provided you’re willing to do your homework.

Product and Service Offerings

Let’s dig into exactly what The Entrust Group has to offer.

Specializing in Self-Directed IRAs

Most people think “IRA” and picture the usual suspects: mutual funds, stocks, or bonds. With Entrust, you’re not confined to those. You can invest in alternative assets while retaining all the same tax advantages of any other IRA.

You can open:

- Traditional Self-Directed IRAs: Funded with pre-tax money. Distributions in retirement are taxed as income.

- Roth Self-Directed IRAs: Funded with post-tax money. Growth and qualified distributions can be tax-free.

- SEP and SIMPLE IRAs: For self-employed individuals or small business owners who want to contribute more than standard IRA limits.

- 401(k) Plans: For small business owners seeking the highest contribution limits and comfortable with the higher cost and administrative burden.

- HSAs and ESAs: If you want to expand beyond retirement-specific accounts, Entrust also offers Health Savings Accounts and Coverdell Education Savings Accounts, both of which can be self-directed.

You make all the investment decisions. Entrust just acts as the recordkeeper and custodian, as required by the IRS.

What Makes Self-Directed IRAs Unique

A Self-Directed IRA (SDIRA) is like a blank canvas for your retirement strategy. Whereas typical custodians let you pick from a handful of pre-packaged options, an SDIRA allows you to get creative.

Whether you’re eyeing a rental property in that up-and-coming neighborhood, or you want to load up on gold bullion because you suspect inflation is on the rise, you can do it with an SDIRA — so long as you follow a few important IRS rules (more on that shortly).

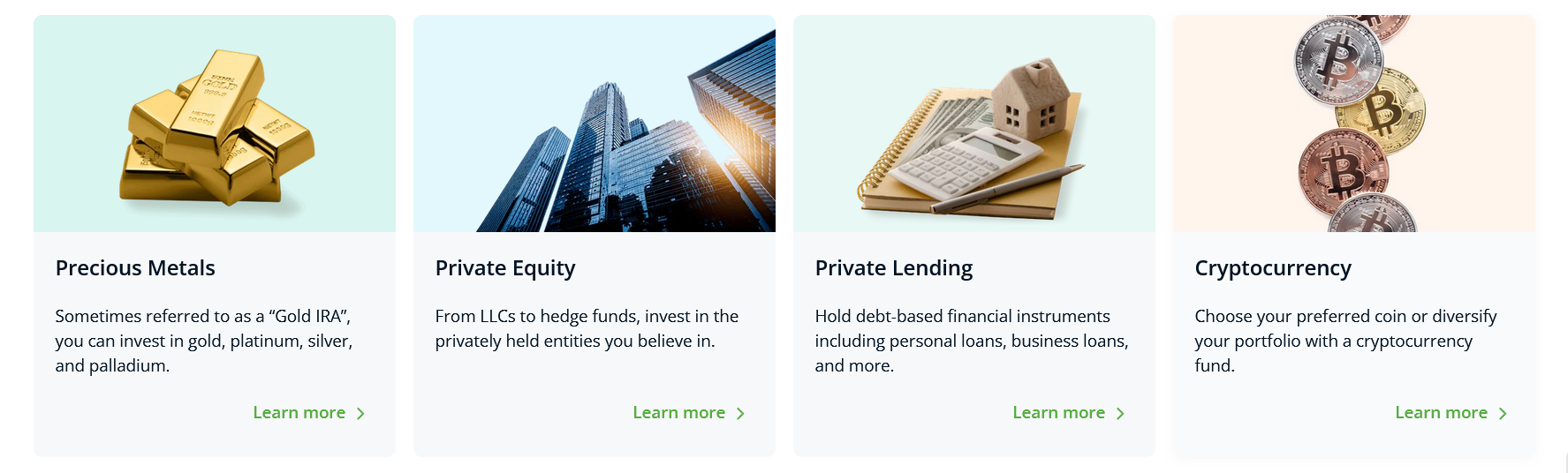

Many investors use Self-Directed IRAs to invest in real estate, but you can also invest in precious metals, private equity, and more:

Along with the freedom to invest in “almost anything,” a few other things come along with the Self-Directed IRA structure:

- You Decide: No more letting a broker handle your future. You’re the captain here.

- Tax Advantages Still Apply: Whether it’s a traditional or Roth structure, your growth gets the usual IRA tax benefits.

- Due Diligence Is On You: This can be both a blessing and a curse. You get the freedom, but you also bear the responsibility if something goes south.

IRS Restrictions and Disqualified Persons

“Almost anything” doesn’t mean everything.

The IRS draws a clear line around certain assets in a Self-Directed IRA:

- Collectibles (most forms of art, antiques, stamps, etc.) are typically off-limits. (Though you can invest in these assets on Public.)

- Life insurance policies are a no-no.

- S-corporations can’t be held in an IRA.

You also can’t transact with “disqualified persons,” like your parents, children, or yourself. That means you can’t buy a beach house via your IRA and then spend your family vacation there.

Entrust won’t micro-manage your choices. It’s on you to be aware of these rules before you invest.

Tools and Education

One of the great things about Entrust is its commitment to investor education.

On the website, you can find video guides and blog posts on everything from investing in car washes and storage businesses inside your IRA, to evaluating private equity investments and the latest updates to IRAs:

Entrust also provides:

- Webinars that demystify IRS regulations.

- Guides on everything from precious metals to farmland.

- Consultations so you can discuss specifics before making big moves.

So if you’re a detail-oriented person who likes to learn, you’ll appreciate the resources they have on tap. You can see them here.

Investment Options

So, what exactly can you invest in?

These are some of the most popular choices:

- Real Estate: Possibly the most popular SDIRA investment. It’s everything from vacation rentals to raw land, from office buildings to farmland.

- Precious Metals: Gold, silver, platinum, palladium — often referred to collectively as “Gold IRAs.”

- Private Equity and Private Lending: You can invest in a local startup or provide a mortgage loan to someone else, turning your IRA into a private bank of sorts.

- Cryptocurrency: With the rise of digital assets, more IRA holders want a slice of the crypto pie.

- Other Alternatives: This can be anything from orchard operations to movie productions — really. If the IRS allows it, you’re good to go.

However, that’s just the start. If you look at the image below, you’ll see 90 different assets you can hold in an SDIRA, from futures to food trucks, farmland, hotels, hedge funds, and more:

This flexibility is precisely why SDIRAs have gained so much traction.

If markets get rocky, or you see a niche opportunity, you’re not constrained by a broker’s limited menu of investments.

Fee Structure

One downside of a self-directed IRA? It’s more paperwork than simply clicking “Buy” on an online brokerage. Real estate transactions, for instance, involve deeds, loan documents, and other complexities. Precious metals might involve storage and shipping.

Processing these transactions requires much more labor and expertise than the automated trading of stocks and bonds — and the fees can reflect that.

Entrust’s fees are structured around transparency and flexibility, so you pay only for what you need:

- Account Establishment Fee: A one-time $50 fee to set up your account.

- Annual Recordkeeping Fee:

- If you hold a single asset under $50,000, it’s $199 a year.

- If you hold multiple assets or your total asset value exceeds $50,000, it’s $299 plus 0.15% of the total asset value above $50k (excluding cash).

- Annual Cap: Recordkeeping fees max out at $2,299 per year, so high-net-worth investors or those with multiple properties won’t be saddled with endlessly growing fees.

- Purchase and Sale Fees: Typically $95 per asset, but it’s $175 if you’re dealing with real estate, and $0 for certain types of transactions (e.g., precious metals, provided you use certain depositories).

- Transaction Fees: Occasional charges might pop up for things like wire transfers, overnight deliveries, or account terminations.

Among SDIRA custodians, these fees are quite competitive, especially given the cap on annual recordkeeping fees. Some custodians might charge lower base fees but tack on incremental charges per asset or per transaction that can escalate quickly.

With Entrust, it’s comforting knowing the absolute most you could possibly pay each year is $2,299 … and you don’t have to worry about any “surprises” exceeding that.

They even have an online fee calculator to help you gauge what you’ll owe annually:

This is super helpful for planning your investments. Many rival custodians bury their fees in complex legal documents or change them year to year. With Entrust, you get consistency and clarity.

Customer Experience

Setting up an account is relatively straightforward. You’ll:

- Open the Account: Fill out the online forms and pay the $50 establishment fee.

- Fund Your SDIRA: Either through a rollover, transfer, or direct contribution.

- Start Investing: Submit an investment direction form for each asset you want to purchase.

Most of the administrative tasks (like transferring money or recording asset deeds) are handled by Entrust, but you must provide clear instructions. Remember, it’s “self-directed,” so they won’t do anything without your say-so.

Customer Support

The Entrust Group prides itself on customer service — a great selling point for any company involved with financial services.

They have a team of highly trained staff who know the ins and outs of IRS rules. In fact, many Entrust team members have earned the Certified IRA Services Professional (CISP) designation, demonstrating mastery of advanced IRA concepts.

If you have a question—like “Is this asset allowed?” or “What’s the best way to roll over funds?”—they’re there to guide you through the process.

It’s worth noting, though, that they’re not financial or tax advisors. They’ll help with compliance questions but won’t give you specific investment advice.

Online Platform Usability

One of the reasons Entrust stands out is its online Entrust Client Portal, which Investopedia has called the “Best Online Portal” in the SDIRA space.

You can:

- Check your account balance 24/7

- View statements

- Monitor assets

- Initiate new investments or sell existing ones

There’s also a mobile app version. So whether you’re at home or on vacation, you can keep an eye on your portfolio. The interface is modern, clean, and user-friendly, which isn’t always the case with financial platforms geared toward alternative investments.

Is The Entrust Group Safe?

Any company that serves as a custodian for IRAs must follow strict IRS guidelines.

Entrust doesn’t actively manage your investments—they’re the administrator—but they’re responsible for recordkeeping, processing transactions, and reporting to the IRS.

They also undergo annual external audits by independent CPAs and conduct regular internal audits for compliance, security, and asset custody.

They operate under federal and state regulations governing IRA custodians, so they’re legit from a compliance standpoint.

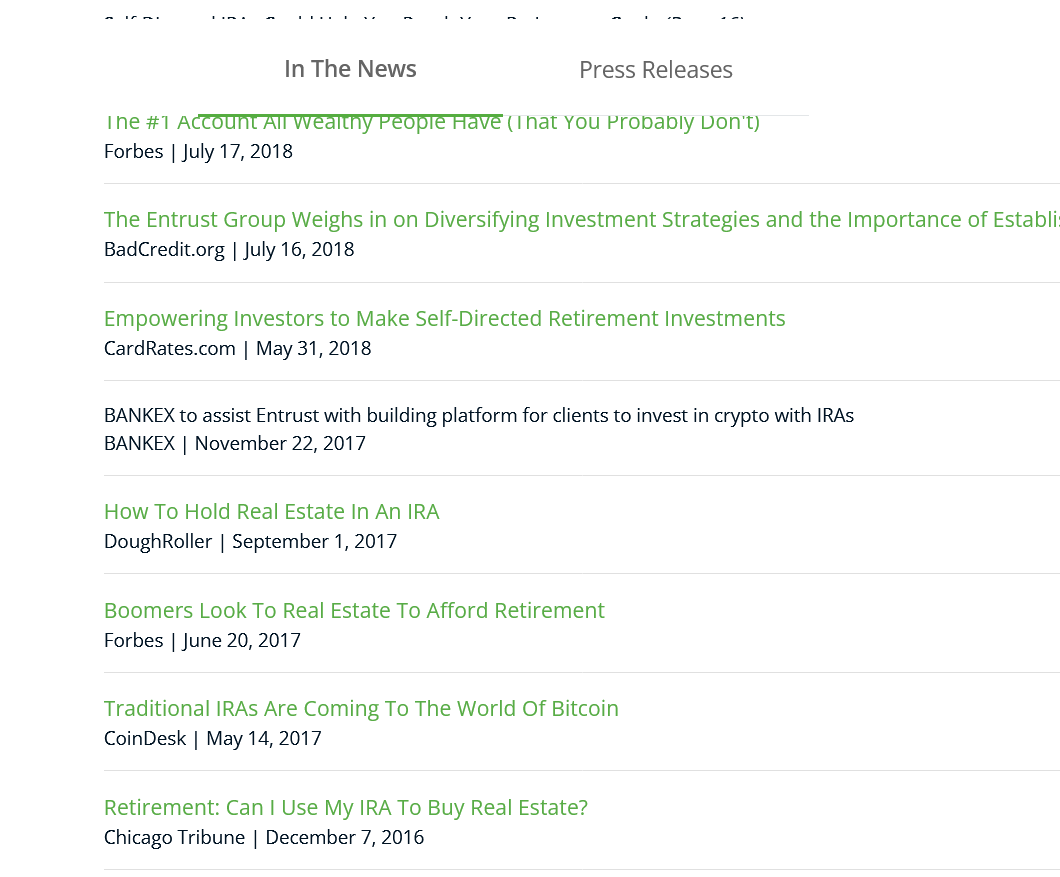

Accreditations and Certifications

- Entrust is a BBB-accredited financial services provider with decades of experience in the industry.

- They’re also frequently recognized in industry publications for their service and robust platform.

For example, the Entrust team is featured in big-name publications like Forbes, Coindesk, and the Chicago Tribune:

While not a guarantee of perfection, these recognitions go a long way in reassuring potential clients that Entrust is both well-established and reputable.

Customer Reviews and Testimonials

Entrust Group reviews and client feedback is generally positive. In reviewing a ton of reviews myself, I’ll distill it down to the key bullet points for you:

- Entrust has high-quality education resources

- Responsive customer support

- It has a user-friendly online portal

On the flip side, some clients mention that the fees can feel high, particularly if you’re only dabbling in smaller, straightforward investments. This is the biggest critique, and it makes sense.

But for many, the fees are more than offset by the ability to invest in lucrative or specialized assets they wouldn’t otherwise have access to in a standard IRA.

Handling Sensitive Financial Data

Security is always a concern when it comes to financial accounts.

Entrust uses encryption, secure servers, and multi-factor authentication to protect client data and transactions. They also have internal protocols for verifying any requests to move funds or assets.

The Entrust Group: Pros and Cons

Strengths

- Variety of Assets: From real estate to crypto to private business and hedge funds, you can diversify like never before.

- Transparency: Their fee schedule is straightforward, with a cap on annual recordkeeping charges.

- Customer Service and Tools: A robust online portal, resource library, and knowledgeable staff.

- Long Track Record: Over 40 years in the business, administering billions in assets.

Weaknesses

- Higher Fees: Compared to standard IRAs, the fees can be substantial. If you don’t intend to invest in a wide variety of assets, you could be paying for more flexibility than you really need.

- Self-Directed Complexity: You’re responsible for compliance, and mistakes could jeopardize your IRA’s tax advantages.

- No Investment Advice: Entrust can’t tell you what to buy or sell, so you’ll need to do your own research.

Who Should Use The Entrust Group?

Self-Directed IRAs from The Entrust Group could be a great fit if you’re dissatisfied with the limited options that traditional accounts offer you.

If you know that you want to invest in real estate, private equity/credit, hedge funds, or private businesses like hotels, self-storage units, car washes, etc. within an IRA, then this is one of the best tax-advantaged ways to do so.

Many types of investors could benefit from this approach, including:

- Real Estate Buffs: If you’ve got a knack for property, an SDIRA can help you tap into that skillset while benefitting from tax-advantaged growth.

- Alternative Asset Enthusiasts: Whether you’re a gold bug or a crypto fan, you can go beyond vanilla mutual funds.

- Those Who Already Have Skin in the Game: Maybe you’re a contractor, landlord, or have a background in small business finance. Use that expertise in your IRA.

- Those Diversifying a Large Portfolio: If you have significant capital and want to reduce your stock market correlation, alternative assets might help smooth out volatility.

Bottom line? With an SDIRA, you cut out many brokerage limitations. If you like forging your own path, this is it.

Final Word:

Is The Entrust Group legit? Absolutely. They’ve operated for over four decades, maintain strong industry credentials, and administer billions in assets … and there are plenty of Entrust Group reviews online. They’re known for excellent customer support, a transparent fee structure, and a robust online portal.

Yes, SDIRAs and an Entrust Group IRA are more expensive and more hands-on than a standard IRA … but that’s the nature of alternative investing. You’re paying for more expertise and more options.

Should you consider it? If you’re an investor who wants full control over your retirement strategy and you’re comfortable navigating the extra complexity (and costs), The Entrust Group is a front-runner worth checking out.

If you’re satisfied investing in individual stocks, ETFs, mutual funds, bonds, and other publicly traded vehicles … then the flexibility and fee structure is probably overkill for you.

SDIRAs are worth considering for anyone who sees untapped opportunities in real estate, private businesses, precious metals, hedge funds, venture capital, or other alternative assets.

It’s not a silver bullet for everyone, but for the right investor, an Entrust IRA can open doors to new asset classes and growth potential. Just be ready to take the driver’s seat in managing your investments, do your due diligence, and embrace the learning curve.

If you want to jump in, grab a free consultation from Entrust or attend one of their webinars.

FAQs:

How does a self-directed IRA work with The Entrust Group?

An Entrust Group self-directed IRA allows investors to diversify their retirement portfolio beyond traditional stocks and bonds by investing in alternative assets like real estate, private equity, and precious metals.

As the custodian, The Entrust Group facilitates transactions and provides account management tools, while investors retain full control over their investment decisions.

How do I contact The Entrust Group?

You can contact The Entrust Group by calling 1-800-392-9653, emailing TEG@theentrustgroup.com, or visiting their website to schedule a free consultation.

Their support team provides education on opening and managing an Entrust Group self-directed IRA, investment rules, and compliance requirements.

Is The Entrust Group legit?

Yes, The Entrust Group is a legitimate and well-established provider of self-directed IRAs, with over 40 years of experience and more than $5 billion in assets under administration.

They are BBB accredited, comply with IRS regulations, and have been recognized for their industry-leading online account management portal.

What are The Entrust Group’s fees?

The Entrust Group self-directed IRA fees include a one-time $50 account setup fee, an annual recordkeeping fee starting at $199, and transaction fees based on the type of investment.

Fees scale with account complexity but are capped at $2,299 per year, making them competitive among self-directed IRA custodians.

Where to Invest $1,000 Right Now?

Did you know that stocks rated as "Buy" by the Top Analysts in WallStreetZen's database beat the S&P500 by 98.4% last year?

Our April report reveals the 3 "Strong Buy" stocks that market-beating analysts predict will outperform over the next year.