Nate is a serial entrepreneur, part-time investor, and founder of WallStreetZen. He holds a Juris Doctor (JD) degree from UAlberta Law - but don’t hold that against him. He’s passionate about building great software that delights users. He occasionally writes about himself in the 3rd person.

I want to live a comfortable life. I also want to do what I can to ensure a comfortable life for my children / future generations. Can you relate?

If you answered yes, let’s get to the important business of how to build generational wealth.

In this article, I dig into the art and science of how to create generational wealth, from how to start to how to continue building family wealth for years to come.

But first…

What is Generational Wealth & Why is it Important?

Before we dig into ways to create generational wealth, let’s talk about what it is and why it matters.

Generational wealth refers to financial assets, property, or investments that are passed down from one generation to the next. Simple as that.

The idea is that by building wealth and accumulating assets that you can pass on, you’ll build a comfortable foundation not only for yourself but also for future generations. This can help break cycles of struggle and allow future generations to pave a more comfortable path in life.

Enabling you to make smarter investment decisions…

Investing in stocks is one of the best ways to build wealth. A Zen Investor subscription gives you access to a market-beating portfolio of stocks, hand-picked by a 40+ year market veteran. Here’s what you get:

✅ Portfolio of up to 30 of the best stocks for the long haul, hand-selected by Steve Reitmeister, former editor-in-chief of Zacks.com with a 4-step process using WallStreetZen tools

✅ Monthly Commentary & Portfolio Updates

✅ Sell Alerts if the thesis changes

✅ Members Only Webinars

✅ 24/7 access to all the elements noted above, and access to an archive of past trades and commentary.

How to Build Generational Wealth

Now that you understand what it is, let’s talk about ways to create generational wealth.

1. Pay Off Debt

High-interest debt is like a noose … you must get it off your neck!

Any debt with a high interest rate can cost you hundreds of dollars in interest alone — and it can compound over time, keeping you in debt and keeping you from growing your net worth.

This can erode your financial potential and limit your ability to build a financial foundation.

So if you have debt, reducing it is precisely how to start building generational wealth. After all, you might actually earn a higher “return” by paying off a debt with a 10% (or higher) interest rate.

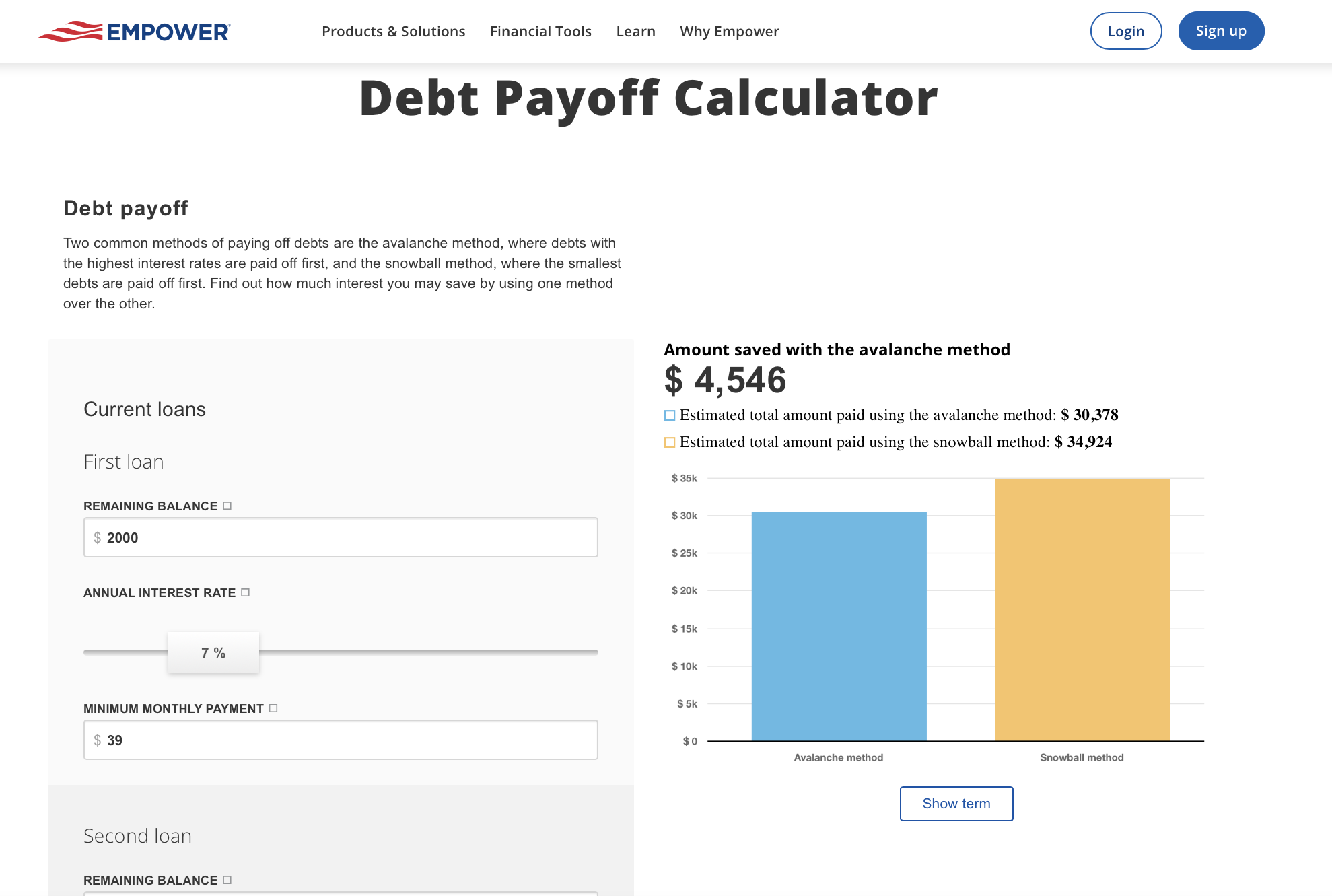

Putting together a debt payoff plan is the best way to become debt-free. One of the best ways to make a plan and stay on track is with a tool like Empower.

Get used to the name, because I’m going to mention Empower a few times in this post. That’s because it’s loaded with FREE tools to help you save and invest smarter — both of which are crucial for building generational wealth.

Specifically related to paying off debt, Empower’s free dashboard has a Debt Payoff Calculator, which lets you enter all of your current loans and interest rates and allows you to build a plan for paying it off.

I can’t recommend this tool enough if you’re struggling with debt. I know it’s not as fun as some of the other tips in this post, but you’ve got to start here if you want to build generational wealth.

2. Start Saving

Starting to save early is essential for building generational wealth because it allows your money to grow through the power of compound interest over time.

Seriously, even small, consistent contributions can add up and compound over time. This makes saving an important part of creating a financial foundation.

Here’s how I suggest getting started:

Set Up a High-Yield Savings Account

One of the easiest ways to start saving — and earning compounding interest — is to set up a high-yield savings account.

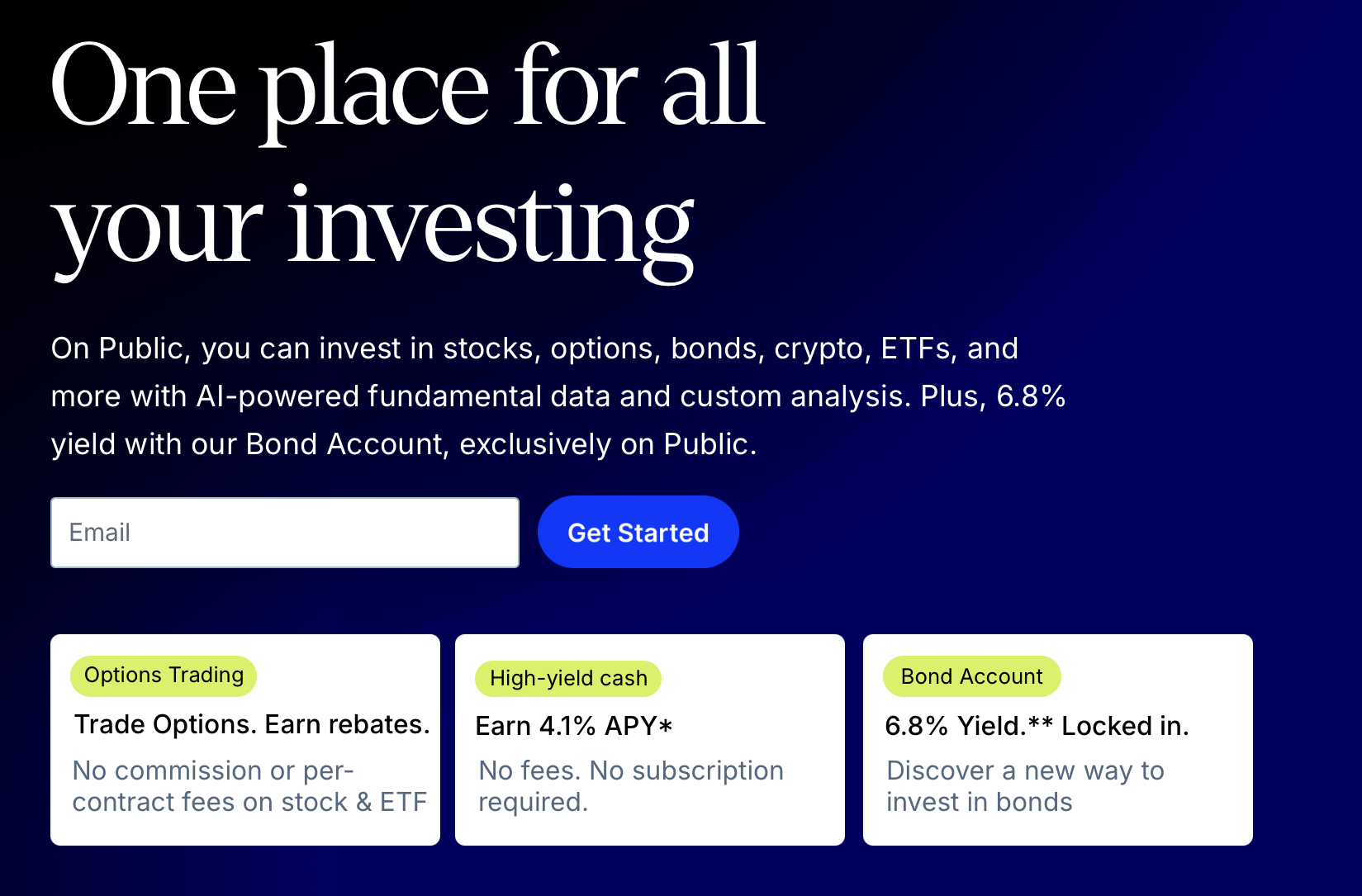

Personally, I like maintaining high-yield savings in an account where I can also invest. If you like that idea too, I suggest checking out Public.

Public is an all-in-one investing platform. For me, its high-yield cash account was the gateway since it offers one of the better APYs out there, and you get daily updates on how much you’ve earned.

(Note: Public’s is not a high-yield savings account — it’s a high-yield cash account, so your money is swept to partner banks. But it’s still FDIC insured, which is what matters most to me.)

Once you have a nice little nest egg built up, you can also invest right on the Public platform. As for what you can invest in, you’ve got options.

You can invest in stocks, ETFs, crypto, and even assets that are hard to find on other brokerages, like T-bills and their nifty Bond account, which allows you to invest in high-quality bonds within a single investment. (Currently, that Bond account yields over 6.8%.)

Save For the Future

Maintaining savings that you can dip into at any given time is great. But if you want to get serious about building generational wealth, you’ve got to adopt a longer mindset.

For most people, there are two key areas to consider when saving for the future:

Save for Future Generations

If you have children or are planning to, now’s the time to start saving for their education and/or future.

There are a variety of ways to do this. One way is to open a 529 account (a tax-advantaged savings plan designed to help pay for education expenses).

Another way is to open an UGMA/UTMA account, which is a custodial account that lets you transfer financial assets to a minor, who gains full control of the funds upon reaching the age of majority. It has fewer restrictions than a 529 plan.

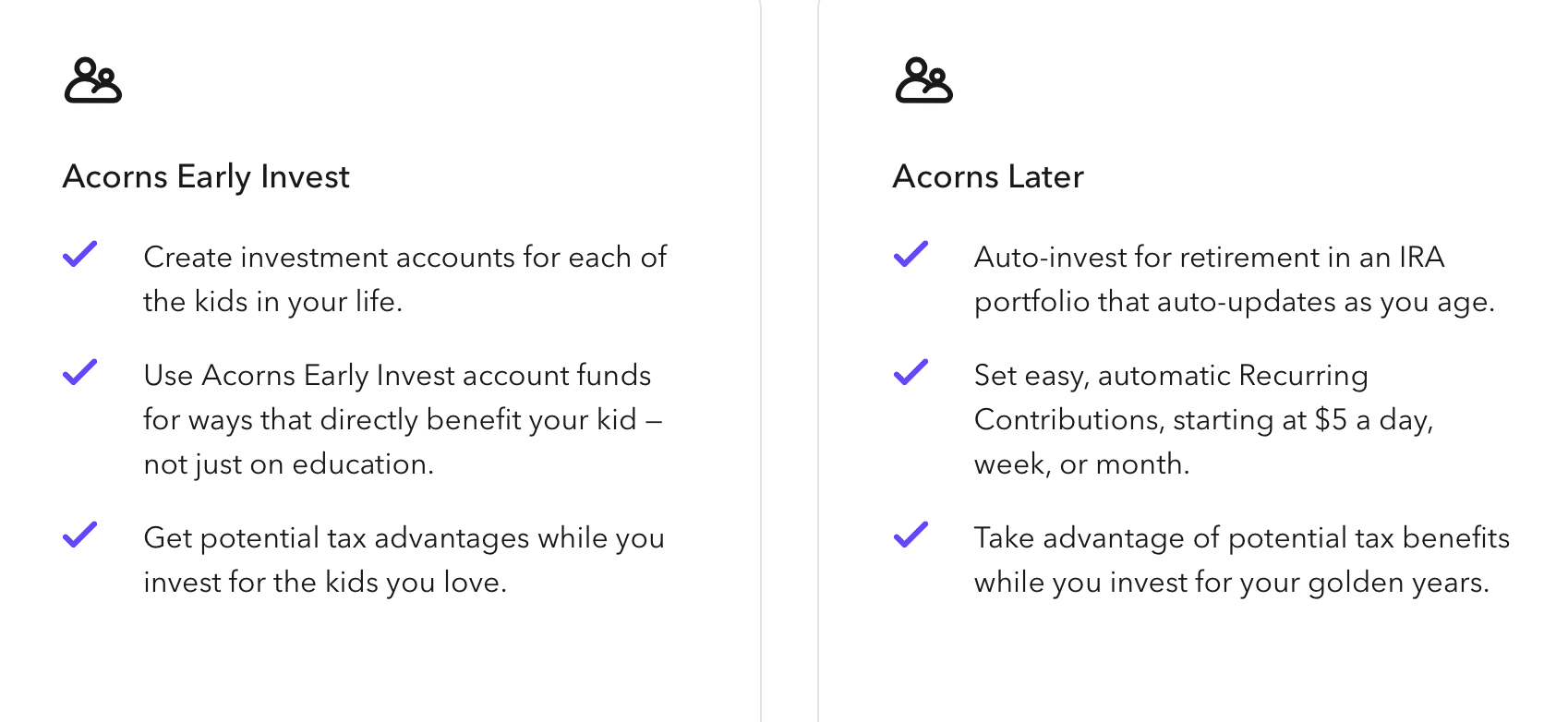

For the latter, I strongly recommend an Acorns Early account.

It’s an UGMA/UTMA investment account within the Acorns app that lets you invest for a child’s future, featuring automated investing — the money is automatically invested for you into a diversified portfolio. (P.S. Acorns also has a retirement account if you want to invest for your future, too.)

You can also link up Acorns to your debit card and round up the change on everyday purchases, which is then deposited into your investment account. This Round-Up feature is a great way to start saving on the sly — you probably won’t miss the rounded-up 52 cents when you buy a latte, but over time these micro-investments add up.

Save for Retirement

Do your future self a solid and save what you can for your golden years. This will ensure that your assets aren’t depleted later on, so you have something to leave

For one, if you have a 401(k), try to contribute all you can — especially if your employer has a matching program.

Additionally, if you don’t already have one, open an IRA. There are a few different types of IRAs — a Traditional IRA, Roth IRA, Simple IRA, Sep IRA, or Best Self Directed IRA. Choose an IRA that is aligned with your goals — if you’re looking for an excellent provider, check out Empower’s available options.

Estate Planning

Nobody likes thinking about death, but you’ll do your family a solid for the future by taking care of the nuts and bolts.

- Create a will and trust: It’s hard to do, but do it. It will make your family’s lives easier later on.

- Plan for tax-efficient wealth transfer: By working with an estate planner in tandem with a financial planner, you can create a plan to efficiently transfer wealth with minimum tax dings. This might include gifting strategies to transfer health and more.

BTW, if you do your own taxes and typically use TurboTax, you might want to consider this offer — H&R Block is offering 20% off DIY taxes. Get the offer here.

3. Start Investing in the Stock Market

On to the fun stuff!

You’ve probably heard that investing in the stock market is a great way to build generational wealth. It can be — but it can also be risky. So it’s important to avoid getting out of your depth.

Above, I mentioned Public as an all-in-one investing resource. I personally use the platform to invest in a high-yield cash account, a Bond account, and select stocks and ETFs. I love it and would recommend it to most people. However, there are two groups who might want to explore other options:

- Total newbies

- More experienced investors who want a greater variety of tools

Don’t worry. I won’t leave you hanging. Here are some potential starting points if you fall into one of those camps.

Beginner Investors

If you’re a brand-new investor, you might like the ease of a platform like Acorns, which allows you to invest automatically.

I’m probably going to bore you by talking about their Round-ups feature again. But seriously — it’s the best. And it can be used for an Early account (referenced above) or for an investment account.

The way it works is simple — your purchases are rounded up to the next dollar and that spare change is invested in your Acorns account.

I usually don’t miss the spare change, and it starts to accumulate over the month, so I feel like I’m saving and investing at once.

Acorns is an automated investment account or robo-advisor. With a basic plan, you’ll simply invest within a strategy that suits your style and risk tolerance, which is determined through a series of questions when you sign up. However, higher-tier memberships allow you to add individual securities to your portfolio.

More Experienced Investors Who Want a Greater Variety of Tools

If you’re a more experienced investor, or if you want a platform that’s more stock-centric, you may want to consider eToro.

It’s our favorite brokerage for a variety of reasons, not least of which are a huge amount of available assets and resources like the Paper Trading feature which allows you to test strategies in real-time without risking money, and the CopyTrader feature which lets you mirror the trades of more experienced investors.

eToro is a multi-asset platform which offers both investing in stocks and cryptoassets, as well as trading CFDs. Please note that CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 51% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work, and whether you can afford to take the high risk of losing your money. This communication is intended for information and educational purposes only and should not be considered investment advice or investment recommendation. Past performance is not an indication of future results. Copy Trading does not amount to investment advice. The value of your investments may go up or down. Your capital is at risk. Cryptoasset investing is highly volatile and unregulated in some EU countries. No consumer protection. Tax on profits may apply. Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you should not expect to be protected if something goes wrong. Take 2 mins to learn more eToro USA LLC does not offer CFDs and makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared by our partner utilizing publicly available non-entity specific information about eToro.

But no matter what platform you choose, you’re responsible for your own investments, so it’s important to have solid tools for stock-picking.

Use the Right Stock Research Tools

Don’t just randomly invest in things you hear about on Twitter. Take the time to do it right.

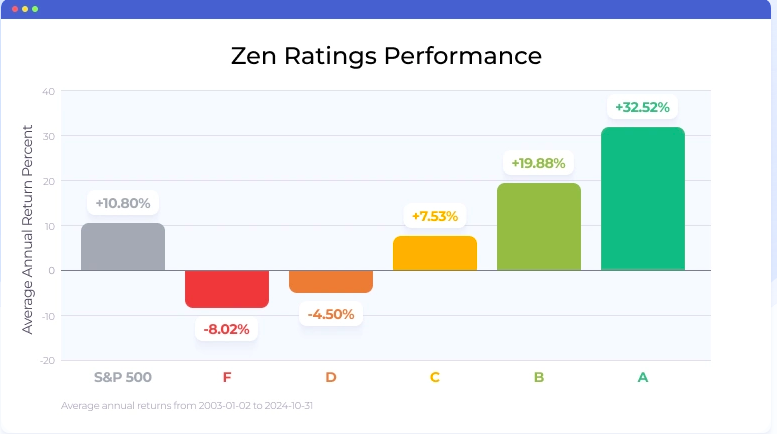

Self-led tools like WallStreetZen can help you locate higher-potential investments. For instance, you can enter any ticker and see its Zen Rating, our quant ratings system that distills 115 factors proven to drive stock growth into an easy-to-read letter grade.

Stocks rated “A” using this system have historically generated 32.52% annual returns — which makes a compelling case for running potential investments through this system to see how they stack up before you execute a trade.

If you feel like you need more guidance, stock-picking newsletter like Zen Investor can also cut down on your research time by leading you more directly to potential investments. This hand-picked portfolio of stocks is curated and managed by Steve Reitmeister, an investor with 40+ years of experience.

4. Invest in More Than Just the Stock Market

You’ve heard the adage “don’t put all your eggs in one basket.” In the investing world, diversification is the way that you spread your eggs among several baskets.

That is to say — don’t just invest in the stock market. After all, the stock market can experience downturns.

You may have heard of the “60/40” portfolio — this classic stock/bond allocation has long been considered the gold standard of investing.

But this classic allocation could leave opportunities (and potential returns) on the table.

Consider a recent study from investment giant KKR that examined the benefits of adding alternative investments into the mix over almost a century of returns. Their findings?

The 40/30/30 portfolio (including real estate, infrastructure, and private credit assets)…

Offered both higher returns — with lower volatility — during periods of high inflation.

The point I’m making? Diversify beyond just stocks and bonds.

You can visit our Best Alternative Investments post for more ideas, but I’ll share just two here:

Real Estate

Most rich people have something in common: They’re also real estate investors.

Yes, you can buy a property and rent it out. But that’s kind of a hassle (trust me, I used to be a landlord). These days, I prefer to invest via real estate investing platforms. In my opinion, it’s the best of both worlds: You get to invest in real estate, but you don’t have to be a landlord.

Different platforms work in different ways, but typically you invest into properties on a fractional basis or via funds.

In my opinion, the gold standard is EquityMultiple. EquityMultiple is a crowdfunded real estate investment platform that gives accredited investors access to professionally managed properties.

The opportunities include a diverse mix of property types and price points. Minimums range from as low as $5,000 to $30,000 depending on the project. You can also invest directly in commercial real estate deals.

The platform boasts $4.4 billion in project value, and the average historical returns are 17% — which far outpaces many other asset classes.

Fees vary depending on the investment; equity investments may charge between 0.5 to 1.5%, which is similar to other crowdfunded real estate platforms.

But hey, what if you’re not accredited?

Another great option is the Yieldstreet Alternative Income Fund (formerly the Prism Fund).

While many of the assets on Yieldstreet are reserved for accredited investors, this fund is available to both accredited and non-accredited investors.

This fund is sort of an all-in-one alternative investment, giving you access to commercial real estate, art, and more for a minimum investment of $10,000. Currently, the AUM is $152 million and the net annualized yield is listed as 8.3%.

I consider the Alternative Income Fund a fantastic way to diversify beyond the stock market and to protect your portfolio during market downturns.

Private Credit

Percent gives accredited investors access to an asset class that I personally think is way under-appreciated: Private credit.

To those not in the know — the private credit market currently stands at over $2 trillion. Yes, with a T.

The short version is that there are a lot of companies out there that don’t have easy access to traditional (ie bank) lending. I won’t get into the why behind that (you can learn more here) but just know that it’s a thing.

Private credit lenders step in to act as the bank in such cases.

While this market used to be reserved for ultra-wealthy or well-connected investors, platforms like Percent have made it accessible to everyday investors with accredited status.

With Percent, you can gain access to either individual credit deals, or get instant diversification with the Percent Blended Note, which allows you to invest in a variety of deals within a single investment vehicle. (It also happens to be one of their most popular offerings.)

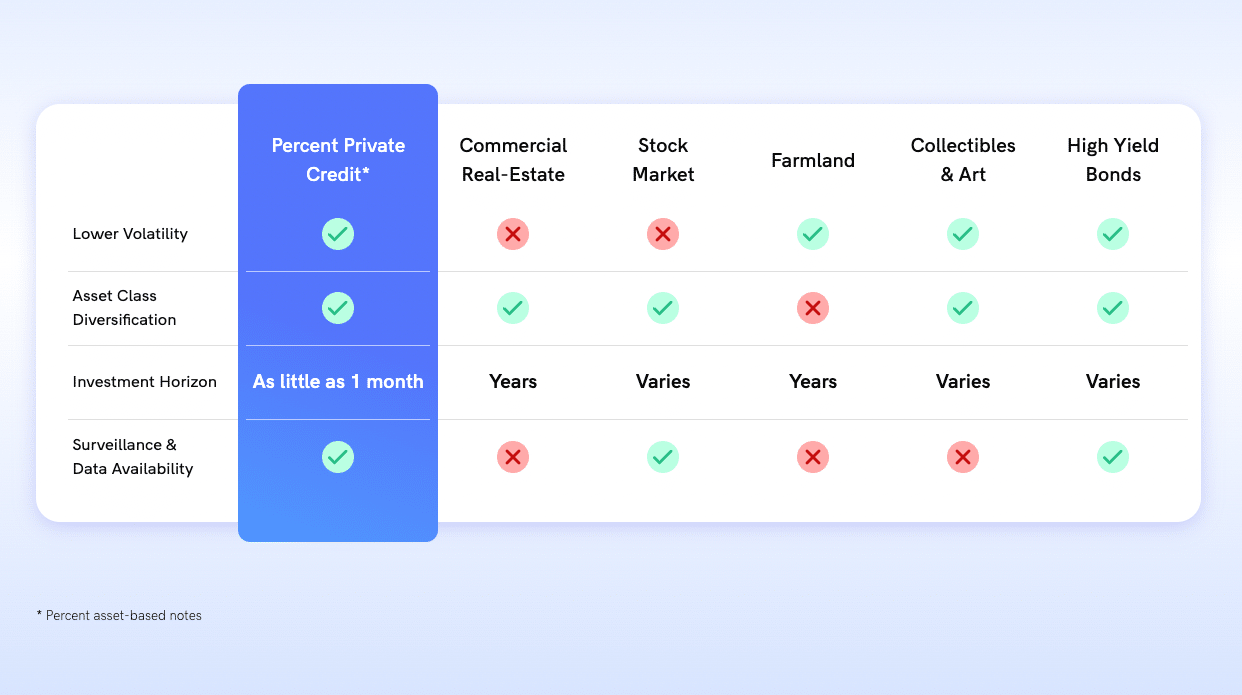

Private credit offers shorter terms than most traditional lending, as well as a higher yield potential. And like real estate, it offers you the chance to diversify beyond stocks.

Regarding that last point, here’s how private credit stacks up against other alternative investment strategies…

To bring the point home: Percent offers access to private credit deals on an easy-to-use (and extremely transparent) platform and makes it easy to find alternative investments that align with all of your portfolio objectives.

Plus, right now, Percent is offering a bonus of up to $500 for your first investment!

5. Teach Financial Literacy

There’s a famous quote. You’ve probably heard it before. It goes: “Give a man a fish, and you feed him for a day; teach a man to fish, and you feed him for a lifetime.”

The point? Education is the key to helping others succeed.

Building generational wealth is not just about developing good habits and acquiring the right asset mix.

It’s also about teaching future generations how to do the same.

This might sound like “duh” stuff, but it’s worth passing on:

As you develop more experience and expertise about investing and saving, share what you learn with your children.

- Educate your children on the basics of saving, investing, and budgeting.

- Use tools like Acorns Early and include beneficiaries in the process.

- Lead by example with good financial habits.

Parting Words…

Before I go, I’d like to share two quotes.

First up: “The earlier you start, the easier it is to accumulate major wealth. Still, it’s never really too late to begin.” – David Bach

Obviously, the sooner you get started saving and investing, the more you can accumulate. But if you’re late to the game, it doesn’t mean it’s not worthwhile.

I didn’t start saving until I was in my 30s. Now I’m in my 40s. Would I have been better off if I started earlier? Yes. But I’ve already made incredible progress. Which leads me to the next quote…

“The big money is not in the buying and the selling, but in the waiting.” – Charlie Munger

Building generational wealth involves a lot of being patient and sticking with it. It’s not a YOLO your money into GameStop sort of thing. By following the steps listed in this post and being consistent, you’re well on your way.

FAQs:

What is the fastest way to create generational wealth?

The fastest way to create generational wealth is to diminish debt, especially high-interest debt, which can erode your financial foundation. From there, saving, investing (in stocks and beyond) and developing financial literacy are key steps you’ll need to build generational wealth, whether it’s from nothing, from modest savings, or wherever you are.

What is the 3 generation rule for wealth?

The “3 generation rule” for wealth suggests that wealth built in the first generation will be squandered by the third. This doesn’t have to be the case. By developing and teaching financial literacy, it is possible to create generational wealth that lasts beyond a generation or two.

How much money do you need to create generational wealth?

The more money you have to start, the easier it is to create generational wealth. That said, it is possible to create generational wealth from nothing. The most important things you need to do are pay off debt, get serious about saving, and invest wisely. These things are simple in theory, but having a plan can be challenging — hence the tips in this post!

What are the four pillars of generational wealth?

While opinions may differ, four pillars that are crucial to generational wealth include intelligent investing, financial planning, teaching financial literacy, and being consistent in your approach.

Where to Invest $1,000 Right Now?

Did you know that stocks rated as "Buy" by the Top Analysts in WallStreetZen's database beat the S&P500 by 98.4% last year?

Our April report reveals the 3 "Strong Buy" stocks that market-beating analysts predict will outperform over the next year.